Mortgage Pre-Approval in Toronto & Durham: A 2025 Homebuyer Guide

Getting pre-approved for a mortgage in Toronto or Durham can be the tipping point between landing your dream home and losing out. Here is something most buyers miss. A pre-approval not only locks in your interest rate for up to 120 days, but it also signals to sellers that you are a serious contender, giving you a clear edge in bidding wars. Forget the old mindset of shopping first and sorting finances later. In the current market, your real advantage starts before you even set foot in an open house.

What Is Mortgage Pre-Approval and Why Does It Matter

A mortgage pre-approval represents a critical first step for homebuyers in Toronto and Durham Region, serving as a financial compass that guides your home purchasing journey. This process provides a clear understanding of your borrowing capacity and signals to sellers that you are a serious, financially prepared buyer.

Understanding the Pre-Approval Fundamentals

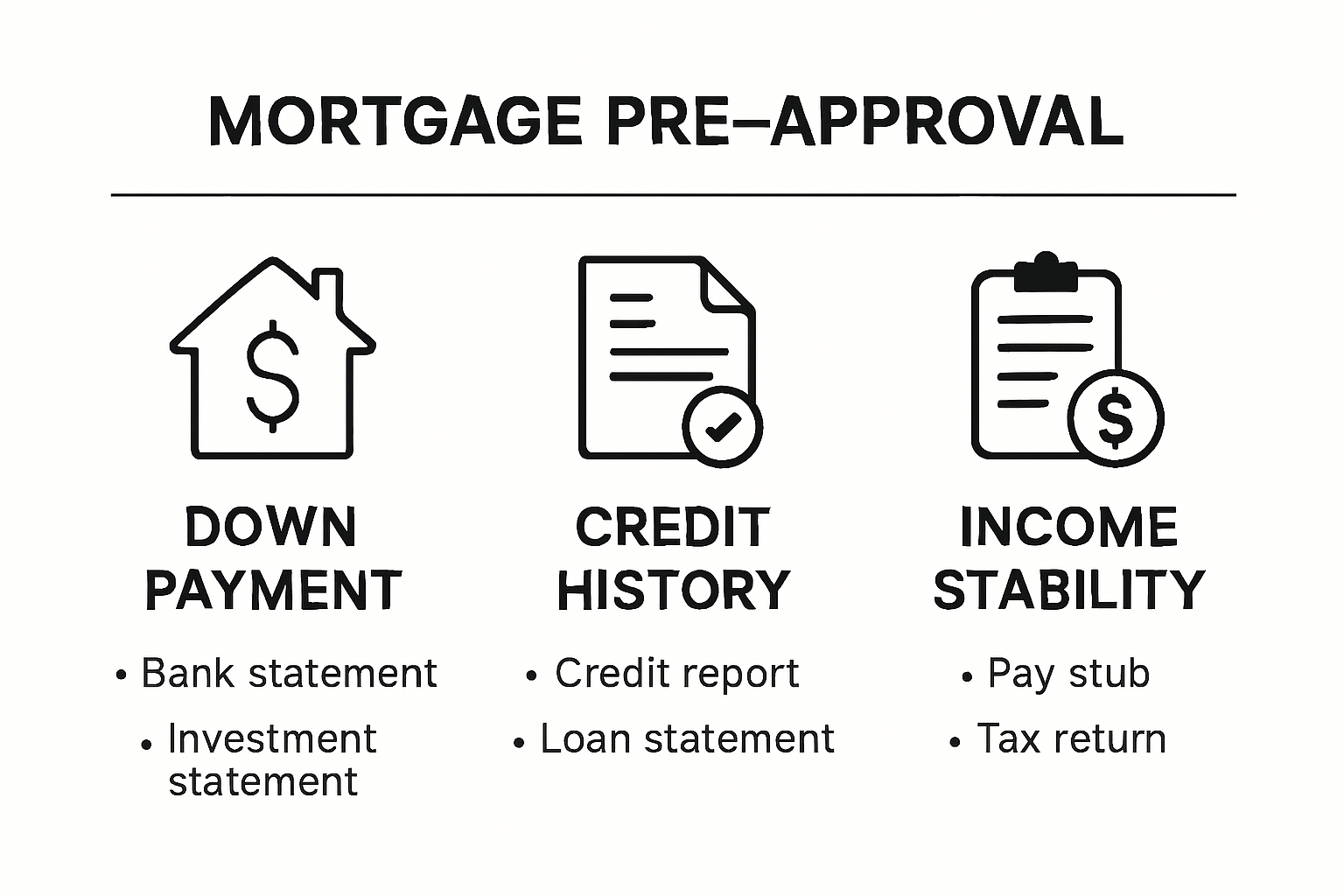

Mortgage pre-approval is a comprehensive financial assessment where lenders evaluate your fiscal health and determine the maximum mortgage amount you qualify for. According to Nerdwallet, this process involves a detailed review of your financial profile, focusing on three fundamental pillars: down payment, credit history, and income stability.

When you seek mortgage pre-approval, lenders will request extensive documentation to validate your financial standing. This typically includes recent pay stubs, tax returns, bank statements, and proof of employment. They conduct a thorough credit check and assess your debt service ratios to determine your borrowing potential. By getting pre-approved, you gain several strategic advantages in the competitive Toronto and Durham real estate markets.

Strategic Benefits of Mortgage Pre-Approval

The advantages of obtaining mortgage pre-approval extend far beyond a simple number. First, pre-approval allows you to lock in an interest rate for a set period, typically between 60 to 130 days. This protection shields you from potential market fluctuations and provides financial predictability. According to Altrua Financial, this rate guarantee can represent significant savings in a volatile market.

Moreover, mortgage pre-approval transforms your home-buying approach from speculative to strategic. Sellers perceive pre-approved buyers as more credible and financially prepared. In competitive markets like Toronto and Durham, this can give you a substantial edge. Your pre-approval demonstrates to real estate agents and sellers that you have already undergone rigorous financial scrutiny and are ready to make a serious offer.

Pre-approval also helps you establish a realistic budget, preventing the disappointment of falling in love with a home outside your financial reach. By understanding exactly how much you can borrow, you can focus your search on properties that align with your financial capabilities. This targeted approach saves time, reduces stress, and increases the likelihood of a successful home purchase.

Remember that mortgage pre-approval is not a guaranteed mortgage loan but rather a strong indication of your borrowing potential. Lenders will conduct a final verification before closing, so maintaining your financial status during the home buying process is crucial.

Remember that mortgage pre-approval is not a guaranteed mortgage loan but rather a strong indication of your borrowing potential. Lenders will conduct a final verification before closing, so maintaining your financial status during the home buying process is crucial. Avoid major financial changes like switching jobs, making large purchases, or opening new credit lines that could impact your pre-approval status.

For homebuyers in Toronto and Durham Region, mortgage pre-approval is more than a procedural step. It is a strategic tool that empowers you with financial clarity, market credibility, and confidence in your home buying journey.

Navigating the mortgage pre-approval process in Toronto and Durham requires strategic preparation and a clear understanding of lender requirements. This comprehensive guide walks you through each critical stage, ensuring you position yourself as a strong, credible homebuyer in the competitive regional real estate market.

Preparing for mortgage pre-approval begins with comprehensive financial documentation. According to the Financial Consumer Agency of Canada, lenders require specific documents to assess your borrowing potential. You will need to compile:

Government Identification: Valid Canadian passport or driver's license

Income Verification: Recent pay stubs, T4 slips, and two years of tax returns

Employment Letter: An Official document confirming your job status and annual income

Bank Statements: Showing savings, investments, and consistent financial activity

Debt Documentation: Current credit card statements, loan balances, and existing financial obligations

For homebuyers in Toronto and Durham Region, mortgage pre-approval is more than a procedural step. It is a strategic tool that empowers you with financial clarity, market credibility, and confidence in your home buying journey.

Step-by-Step Guide to Getting Pre-Approved in Toronto & Durham

Navigating the mortgage pre-approval process in Toronto and Durham requires strategic preparation and a clear understanding of lender requirements. This comprehensive guide walks you through each critical stage, ensuring you position yourself as a strong, credible homebuyer in the competitive regional real estate market.

Gathering Essential Financial Documentation

Preparing for mortgage pre-approval begins with comprehensive financial documentation. According to the Financial Consumer Agency of Canada, lenders require specific documents to assess your borrowing potential. You will need to compile:

Government Identification: Valid Canadian passport or driver's license

Income Verification: Recent pay stubs, T4 slips, and two years of tax returns

Employment Letter: An Official document confirming your job status and annual income

Bank Statements: Showing savings, investments, and consistent financial activity

Debt Documentation: Current credit card statements, loan balances, and existing financial obligations

Understanding the Pre-Approval Application Process

The pre-approval journey involves multiple strategic steps. TD Bank recommends initiating the process online or through an in-person consultation with a mortgage professional. During this stage, lenders conduct a comprehensive financial assessment focusing on three key areas: income stability, credit history, and down payment potential.

Your credit score plays a pivotal role in determining pre-approval eligibility. Most lenders prefer a credit score of 680 or higher, though some may consider scores around 600. Before applying, review your credit report for accuracy and address any potential discrepancies. Learn more about preparing for your home purchase to ensure you present the strongest financial profile possible.

Navigating Rate Locks and Final Considerations

Once pre-approved, lenders typically offer a rate guarantee lasting 60 to 120 days. This window provides critical protection against market fluctuations and gives you time to find the perfect home. However, it is essential to understand that pre-approval does not guarantee final mortgage approval. The actual mortgage amount will depend on the specific property's value and your down payment at purchase time.

During the pre-approval period, maintain financial stability. Avoid major life changes that could impact your creditworthiness, such as:

- Changing employment

- Making large purchases on credit

- Opening new credit accounts

- Significantly altering your existing debt profile

For homebuyers in Toronto and Durham Region, mortgage pre-approval represents more than a procedural step. It is a strategic tool that provides financial clarity, market credibility, and a structured pathway to homeownership. By understanding and methodically executing each stage of the pre-approval process, you position yourself as a serious, prepared buyer ready to navigate the dynamic local real estate landscape.

How Pre-Approval Helps Homebuyers, Sellers, and Investors

Mortgage pre-approval serves as a powerful strategic tool that transforms the real estate experience for homebuyers, sellers, and investors across Toronto and Durham Region. By understanding its multifaceted benefits, each stakeholder can leverage this process to achieve their unique financial objectives.

Benefits for Homebuyers

For homebuyers, mortgage pre-approval is more than a financial formality. According to Northwood Mortgage, it provides a critical framework for preventing financial strain and potential future foreclosure. Pre-approval offers homebuyers precise insights into their borrowing capacity, enabling them to set realistic expectations and develop a targeted home search strategy.

The competitive edge gained through pre-approval cannot be overstated. In Toronto and Durham's dynamic real estate markets, sellers frequently receive multiple offers. Understand how to strengthen your home buying journey by presenting a pre-approval letter, which signals financial readiness and commitment. This document effectively communicates to sellers that you are a serious, qualified buyer prepared to complete the transaction.

Advantages for Sellers and Real Estate Professionals

Sellers benefit significantly from engaging with pre-approved buyers. Durham Mortgage highlights that pre-approved buyers represent lower transaction risks. These potential purchasers have already undergone rigorous financial scrutiny, reducing the likelihood of last-minute financing failures that could derail a sale.

Real estate professionals also appreciate pre-approved buyers. A pre-approval letter streamlines the negotiation process, allowing sellers to confidently evaluate offers knowing the buyer has demonstrated financial capability. This transparency accelerates transaction timelines and minimizes uncertainty for all parties involved.

Strategic Considerations for Investors

Real estate investors find particular value in mortgage pre-approval. TD Bank notes that pre-approval allows investors to lock in interest rates for up to 120 days. This protection shields investors from market volatility and provides a window to identify and secure promising investment properties without risking unexpected rate increases.

Pre-approval enables investors to quickly assess potential investment opportunities against their confirmed borrowing capacity. By understanding exactly how much they can finance, investors can rapidly evaluate properties, make competitive offers, and capitalize on time-sensitive market opportunities in Toronto and Durham Region.

Whether you are a first-time homebuyer, an experienced seller, or a strategic real estate investor, mortgage pre-approval represents a powerful tool in your financial arsenal. It provides clarity, credibility, and confidence, transforming the complex real estate landscape into a navigable pathway toward your property goals.

Expert Tips for Successful Mortgage Pre-Approval in 2025

Successful mortgage pre-approval in 2025 demands strategic financial planning and a nuanced understanding of the evolving real estate landscape in Toronto and Durham Region. Homebuyers must navigate a complex financial ecosystem with precision and foresight to secure optimal lending terms.

Optimizing Your Financial Profile

Preparing for mortgage pre-approval begins with a comprehensive financial assessment. According to Altrua Financial, the three fundamental pillars of mortgage qualification are down payment, credit history, and income stability. Lenders will scrutinize these elements to determine your borrowing potential.

To position yourself as an ideal candidate, focus on improving your credit score. Aim for a score of 680 or higher, which signals financial reliability to potential lenders. This involves maintaining low credit utilization, making consistent on-time payments, and addressing any outstanding credit issues. Learn strategies to protect yourself in the mortgage process and ensure your financial reputation remains pristine.

Strategic Documentation and Financial Preparation

Documentation plays a critical role in mortgage pre-approval. Gather comprehensive financial records that demonstrate your fiscal responsibility. This includes:

- Detailed employment verification letters

- Two years of tax returns

- Recent pay stubs

- Bank statements showing consistent savings

- Documentation of additional income sources

- Comprehensive debt statements

Navigating Potential Lending Challenges

The 2025 mortgage landscape presents unique challenges for homebuyers. Economic volatility and changing lending standards require a proactive approach. Avoid major financial changes during the pre-approval process that could compromise your application. This means:

- Maintaining current employment

- Avoiding large credit purchases

- Minimizing new credit applications

- Keeping existing credit accounts stable

For homebuyers in Toronto and Durham Region, mortgage pre-approval is more than a procedural step. It is a strategic financial maneuver that requires careful planning, meticulous documentation, and a forward-thinking approach. By understanding the intricacies of the 2025 lending landscape, you can position yourself as a strong, credible buyer ready to navigate the complex real estate market with confidence and precision.

Frequently Asked Questions

What is mortgage pre-approval?

Mortgage pre-approval is a financial assessment conducted by lenders to determine how much you can borrow for a mortgage. It evaluates your credit history, income stability, and down payment amount, providing a clear understanding of your borrowing capacity.

How long is a mortgage pre-approval valid for?

A mortgage pre-approval is typically valid for 60 to 120 days. This rate lock period protects you from market fluctuations while you search for a suitable home.

Why is getting pre-approved important for homebuyers in Toronto and Durham?

Getting pre-approved shows sellers that you are a serious buyer, enhances your credibility, and helps you set a realistic budget for your home search, giving you a competitive edge in bidding wars.

What documents are required for mortgage pre-approval?

You will need to provide several key documents, including government ID, recent pay stubs, tax returns, bank statements, and a letter from your employer verifying your income. These documents demonstrate your financial stability to the lender.

Ready to Turn Your Mortgage Pre-Approval Into a Winning Move?

You have learned how critical mortgage pre-approval is in Toronto and Durham. It is your key to unlocking the perfect home, standing out in bidding wars, and locking in the rates you need. Yet finding the right property and navigating your next steps can feel overwhelming if you are doing it alone. With the competitive edge that pre-approval brings, now is the time to use your momentum and make every step count.

Fanis Makrigiannis and the Fanis.ca team are here to bridge the gap between your financial confidence and your future home. Explore exclusive property listings, gain local market insights, and leverage proven strategies tailored just for buyers in Toronto and Durham. Ready to take action and secure your advantage? Connect directly with Fanis today and let a dedicated Realtor® help you transform your pre-approval into a successful home purchase—before another opportunity passes you by.

Contact me personally to learn more.

About the author:

Fanis Makrigiannis is a trusted Realtor with RE/MAX Rouge River Realty Ltd., specializing in buying, selling, and leasing homes, condos, and investment properties. Known for his professionalism, market expertise, and personal approach, Fanis is committed to making every real estate journey seamless and rewarding.

He understands that each transaction represents a significant milestone and works tirelessly to deliver outstanding results.

With strong negotiation skills and a deep understanding of market trends, Fanis fosters lasting client relationships built on trust and satisfaction.

Proudly serving the City of Toronto • Ajax • Brock • Clarington • Oshawa • Pickering • Scugog • Uxbridge • Whitby • Prince Edward County • Hastings County • Northumberland County • Peterborough County • Kawartha Lakes

Fanis Makrigiannis

Real Estate Agent

RE/MAX Rouge River Realty LTD

(c): 905.449.4166

(e): info@fanis.ca

Recommended Articles

Home Buying Process in Toronto & Durham Region for 2025 - Fanis Makrigiannis Realtor®First Home Checklist: Toronto and Durham Region 2025 - Fanis Makrigiannis Realtor®

Your Step-by-Step Guide to Buying a Home - Fanis Makrigiannis Realtor®